Portfolio Update: Adding Adobe

We are adding Adobe to the portfolio as a starter position.

We are adding Adobe to the portfolio as a starter position.

Adobe develops software for creative professionals, businesses, and consumers.

Its main products sit across graphic design, video editing, photography, digital documents, marketing, and content workflows.

Creative Cloud includes products such as Photoshop, Illustrator, Premiere Pro, and After Effects. Document Cloud includes Acrobat and PDF tools. Experience Cloud helps businesses manage digital marketing and customer experiences.

Most revenue is subscription-based.

That gives Adobe a large recurring revenue base, high visibility, strong margins, and significant cash generation.

The business is deeply embedded in professional workflows.

Files, skills, collaboration processes, customer systems, and industry standards have been built around Adobe products over many years.

That creates real switching costs.

Ticker: ADBE 0.00%↑

Decision: Starter position

Initial Sizing: 2%

Entry Price: $204.78

Price Target - Base Case: $440

This is a starter position.

The valuation is highly attractive, but the thesis still depends partly on a future rerating and continued evidence that AI strengthens the platform rather than weakening it.

Why We Are Adding

The thesis has strengthened.

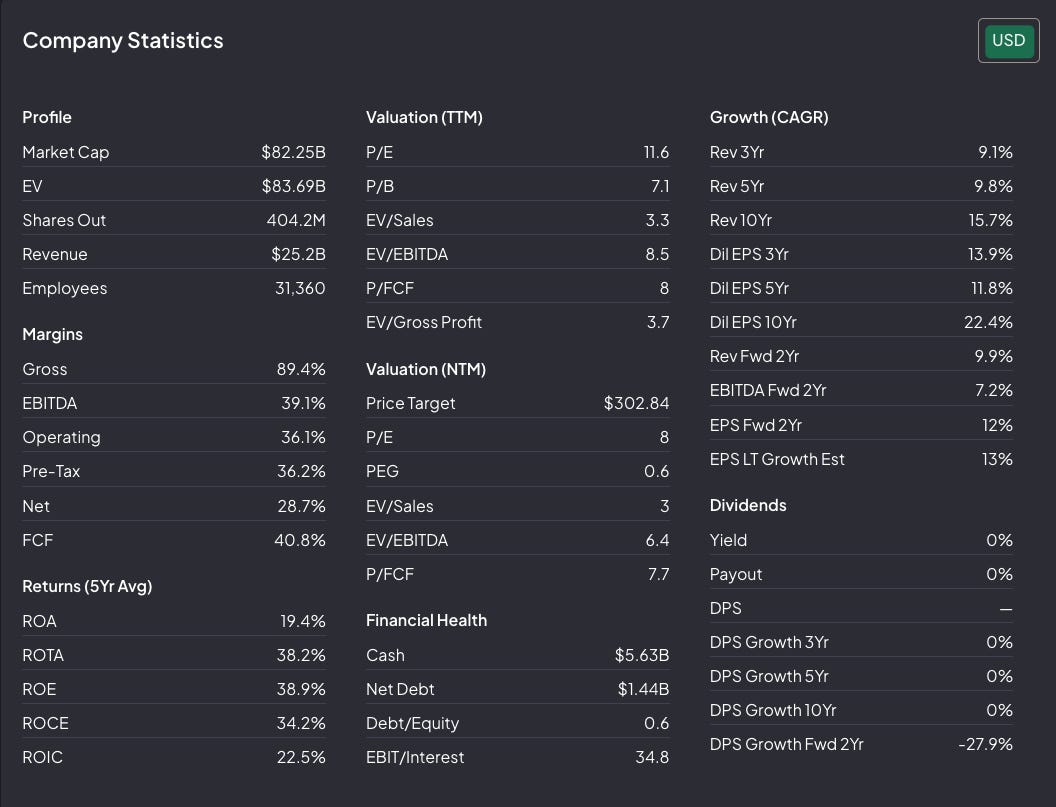

Q2 FY2026 revenue reached a record $6.62 billion, up 13% year over year.

Subscription revenue was $6.42 billion.

Total ARR reached $27.10 billion.

AI-first ARR more than tripled year over year and exceeded $500 million.

Management also raised FY2026 guidance to $26.50–$26.60 billion of revenue and non-GAAP EPS of $24.35–$24.45.

These are not the numbers of a franchise already being displaced.

The business is not simply surviving but it is still growing at a healthy rate while beginning to monetize AI.

That does not remove the risk, but it reduces the probability that Adobe is facing immediate structural collapse.

The Bet

The market is treating Adobe as if generative AI will commoditize creative tools and move value away from the application layer.

That may be partly correct.

AI lowers the cost of creating images, video, and other digital content. New competitors can enter faster. Some users may need fewer traditional editing tools.

But Adobe owns more than an interface.

It has professional workflows, file formats, distribution, customer relationships, enterprise integrations, creative standards, and a large installed base.

AI can reduce the value of individual features.

It can also increase the amount of content created, edited, managed, verified, and distributed through Adobe’s ecosystem.

The bet is that Adobe remains a central platform even as the method of content creation changes.

At the current price, we do not need Adobe to return to peak valuation multiples.

We need the core business to remain healthy, free cash flow per share to grow, and the market to stop pricing the company like an inevitable AI casualty.

What Can Go Wrong

The pre-mortem is:

It is 2031 and the investment disappointed because AI shifted too much value away from Adobe. Users created content directly through general AI systems. Editing tools became less differentiated. New competitors offered good-enough workflows at lower prices. Adobe’s AI products grew, but not enough to offset pressure on the core.

Adobe remained profitable, but the future return became mediocre.

That is the risk.

Invalidation

The thesis weakens if two or more of the following occur:

Subscription growth slows structurally.

Creative workflows move materially outside Adobe.

AI monetization fails to offset erosion in the core.

Margins and free cash flow compress persistently.

Execution quality deteriorates after the CFO transition.

The share count stops falling despite continued buybacks.

One weak quarter would not automatically break the thesis.

A pattern of weakening economics would.

We are starting with 2%.