Portfolio Update: Adding Intuit

We are adding Intuit to the portfolio as a starter position.

We are adding Intuit to the portfolio as a starter position.

The company builds software and financial services for consumers, small businesses, and mid-market companies.

Its main products include TurboTax, QuickBooks, Credit Karma, Mailchimp, and Intuit Enterprise Suite. The business monetises through subscriptions, tax services, payroll, payments, bill pay, capital, marketing tools, and workflow services.

The core value proposition is simple:

Help customers reduce admin work, avoid errors, save time, and manage financial workflows in one platform.

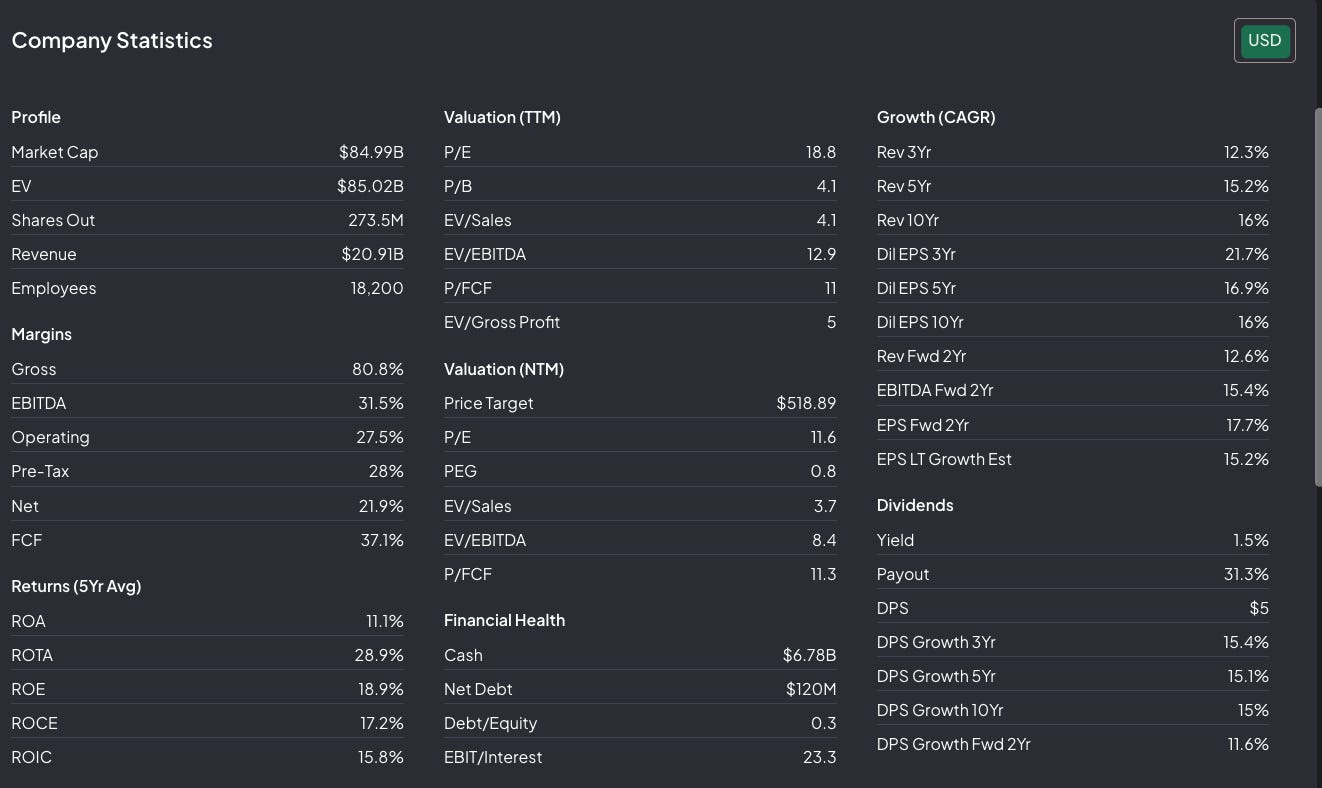

Ticker: INTU 0.00%↑

Decision: Starter position

Initial Sizing: 2%

Entry Price: $315,50

Fair Value Target: $520

This is a starter position, not a full allocation.

The quality is high.T

The balance sheet is solid.

The business is still growing.

But the AI risk is real enough to respect.

Why We Are Adding

The market is treating many software companies as if AI will compress the entire application layer.

That may be too broad.

Intuit’s core business is embedded. It has customer data, financial history, compliance workflows, payroll, payments, and daily operating habits. In that context, AI can make the platform more useful instead of replacing it.

Recent results do not show a broken business:

Q2 FY26 revenue grew 17%.

Global Business Solutions grew 18%.

Online Ecosystem grew 21%.

GAAP operating income grew 44%.

The company also reiterated annual guidance and continues to position itself as an integrated financial platform for SMB, consumer, and mid-market customers.

That is the key point.

The stock price has fallen materially, but the fundamental thesis has not deteriorated in the same way.

The Bet

The return source is a combination of three things:

FCF per share growth.

Moderate rerating from depressed multiples.

The market slowly realising that AI may not destroy Intuit’s core economics.

This is not a distressed valuation.

We are not buying a hated deep value stock.

We are buying a high-quality compounder after a reset in expectations.

What Can Go Wrong

The main risk that Intuit becomes less special.

The pre-mortem is:

It is 2029 and this investment disappointed because the market was right to separate the strong pieces from the vulnerable ones. AI made tax DIY and parts of marketing more commodity. Mid-market execution was harder than expected. Agents reduced the value of the interface. Upsell did not offset pricing pressure. QuickBooks kept growing, but not fast enough to prevent a structural derating.

In that world, Intuit remains a good company.

But the stock delivers mediocre returns.

That is the risk.

Invalidation

The thesis breaks if we see clear evidence that QuickBooks is losing relevance as a system of record and system of work.

Other red-line signals:

Retention, attach, or core monetisation deteriorate.

Margins and free cash flow compress structurally.

AI shifts workflow economics outside Intuit’s platform.

Consumer tax or marketing weakness spreads into the SMB core.

Growth slows without a clear reinvestment explanation

We are starting with 2%.