Portfolio Update: Adding Microsoft Corporation

We are adding Microsoft to the portfolio as a starter position.

We are adding Microsoft to the portfolio as a starter position.

Ticker: MSFT 0.00%↑

Decision: Starter

Entry price: $362.62

Initial sizing: 2%

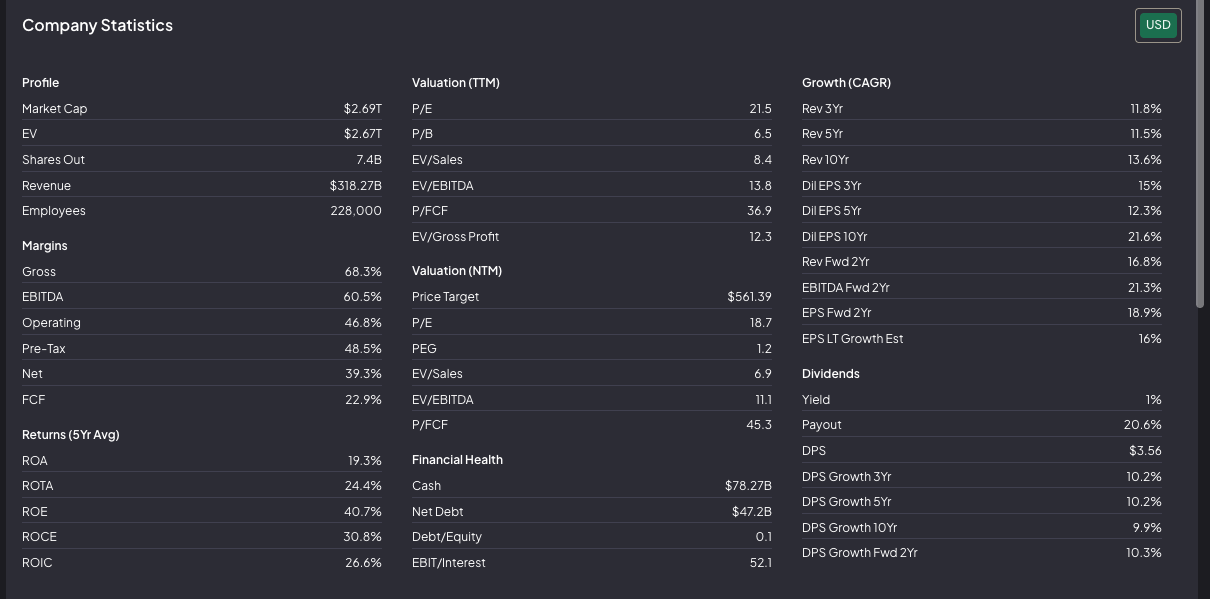

Price Target: $710

This is a starter position.

Microsoft remains one of the highest-quality public businesses in the world. But the AI capex cycle makes the free cash flow picture more complex.

Why We Are Adding

In Q3 FY2026, Microsoft revenue grew 18%, operating income grew 20%, EPS grew 23%, and Azure plus other cloud services grew 40%. Microsoft Cloud reached $54.5 billion in quarterly revenue, up 29% year over year.

The stock price has fallen, but the fundamentals have not shown a clear break.

Green Flags

The business is still growing at a high rate for its size.

Azure remains the key engine. Microsoft Cloud continues to scale. Microsoft 365, security, and AI tools create multiple monetization layers across the same customer base.

The economics are still excellent.

Microsoft also has one of the strongest distribution advantages in enterprise software.

It already sits inside the workflow of millions of businesses. That gives it an enormous advantage when selling AI tools, copilots, security, cloud services, and data products.

Red Flags

The biggest risk is capex.

Microsoft is spending heavily to support AI and cloud growth. If those investments do not produce attractive incremental returns, free cash flow conversion will disappoint.

The valuation is also not low on free cash flow.

Current P/FCF TTM is around 36.9x. That is still demanding, especially for a company becoming more capital intensive.

So, there is also multiple compression risk.

If the market starts valuing Microsoft less like an asset-light software company and more like a capital-intensive AI infrastructure platform, the multiple can come down even if revenue keeps growing.

What Can Go Wrong

The pre-mortem is:

It is 2031 and Microsoft delivered mediocre returns because the market was right to worry about AI capex. Azure kept growing, but growth slowed. AI revenue was real, but not profitable enough. Data-centre investment stayed high. Free cash flow lagged accounting earnings. Returns on capital declined. The multiple compressed.

Final Decision

Microsoft remains a real quality compounder.

At $362.62, it is not a bargain, but it is back in a range where expected returns are reasonable for a long-term investor.

It also trades well below our bear value scenario in year 5.

This looks like a reasonable setup: the business can potentially deliver around 15% per year over time if the base case plays out, with a dividend that can continue growing alongside earnings.

We think MSFT 0.00%↑ is a great company temporarily priced in a way that gives the investor a better margin of safety than usual.

We are opening with 2%.