Research Note #03 — $AAVE

A study of quality, price, odds, and sizing.

Some ideas deserve attention before they deserve capital.

This series is where we study one asset at a time, define the risk, and decide what price would make the bet worth taking.

This is not financial advice.

This week’s Research Note is about:

Aave — $AAVE

1. Why We Are Watching It

We are watching Aave because:

It is one of the strongest lending protocols in DeFi.

It has real usage, real fees, and deep liquidity.

Its token economics are improving through buybacks, but are still not perfect.

The simple thesis:

Aave may become one of the core credit layers of crypto, but $AAVE only becomes attractive if protocol success keeps turning into token-level value.

The key question:

Does Aave’s revenue actually accrue to $AAVE holders, or does the token remain mostly governance plus narrative?

2. What It Does

Aave is a decentralized lending protocol.

Users can deposit crypto assets, borrow against collateral, and earn or pay interest without using a bank.

It creates value through:

Network usage: people use Aave to lend, borrow, refinance, and manage onchain liquidity.

Liquidity depth: Aave’s strength is not just users. It is capital depth, trust, integrations, collateral support, and risk management.

Fees and protocol revenue: Aave generates lending-related fees, but not all gross fees should be treated like equity-like revenue.

Token utility and governance: $AAVE is tied to governance, safety, incentives, and now a protocol-funded buyback program.

The key distinction:

Aave the protocol is clearly useful.

$AAVE the token still needs clean value capture.

3. What We Like

The attractive parts:

Real product-market fit: Aave is not a story-only token. It is used. It has deposits, loans, collateral, fees, integrations, and market share.

Strong competitive position: the moat is liquidity, trust, risk management, integrations, multi-chain distribution, and collateral depth. That is hard to copy quickly.

Improving tokenomics: Aave has a protocol-funded buyback program ($50M annual budget, with weekly purchases between $250k and $1.75M). The important detail: bought tokens are not burned. They go to the Ecosystem Reserve, so this is more like DAO-controlled capital recycling than pure buyback-and-burn.

4. What Scares Us

The risks:

Token value capture risk: Aave can grow while $AAVE underperforms if fees do not translate into durable token demand, scarcity, or direct economic benefit.

Buybacks may not be enough: Delphi’s report is very clear: buybacks are a mechanism, not a moat. Token performance depends on buybacks relative to float, unlocks, traction, revenue, and protocol direction.

Lending is cyclical: Fees are tied to leverage, collateral volatility, borrow demand, liquidations, and crypto market activity. We should not capitalize peak fees as if they are stable earnings.

Competition is real: Morpho, Spark, Compound, Maple, Fluid, and other lending models can pressure spreads, improve capital efficiency, and take share in certain user segments.

5. Quality Score

Business / Asset Quality — 4/5

Durability: strong

Competitive advantage: strong

Market position: strong

Revenue quality: good, but cyclical

Resilience: good, but tied to DeFi market activity

Financial / Economic Quality — 3.5/5

Fees: real

Unit economics: improving

Balance sheet / treasury: relevant but governance-dependent

Margin structure: attractive in theory

Reinvestment potential: strong through GHO, V4, integrations, and ecosystem growth

The haircut is because gross fees are not the same as token-accretive cash flow.

Network Quality — 3.5/5

Developer activity: strong

Network security: strong

Token design: improving

Governance: mature, but still a risk

Ecosystem strength: strong

Total Score

11/15

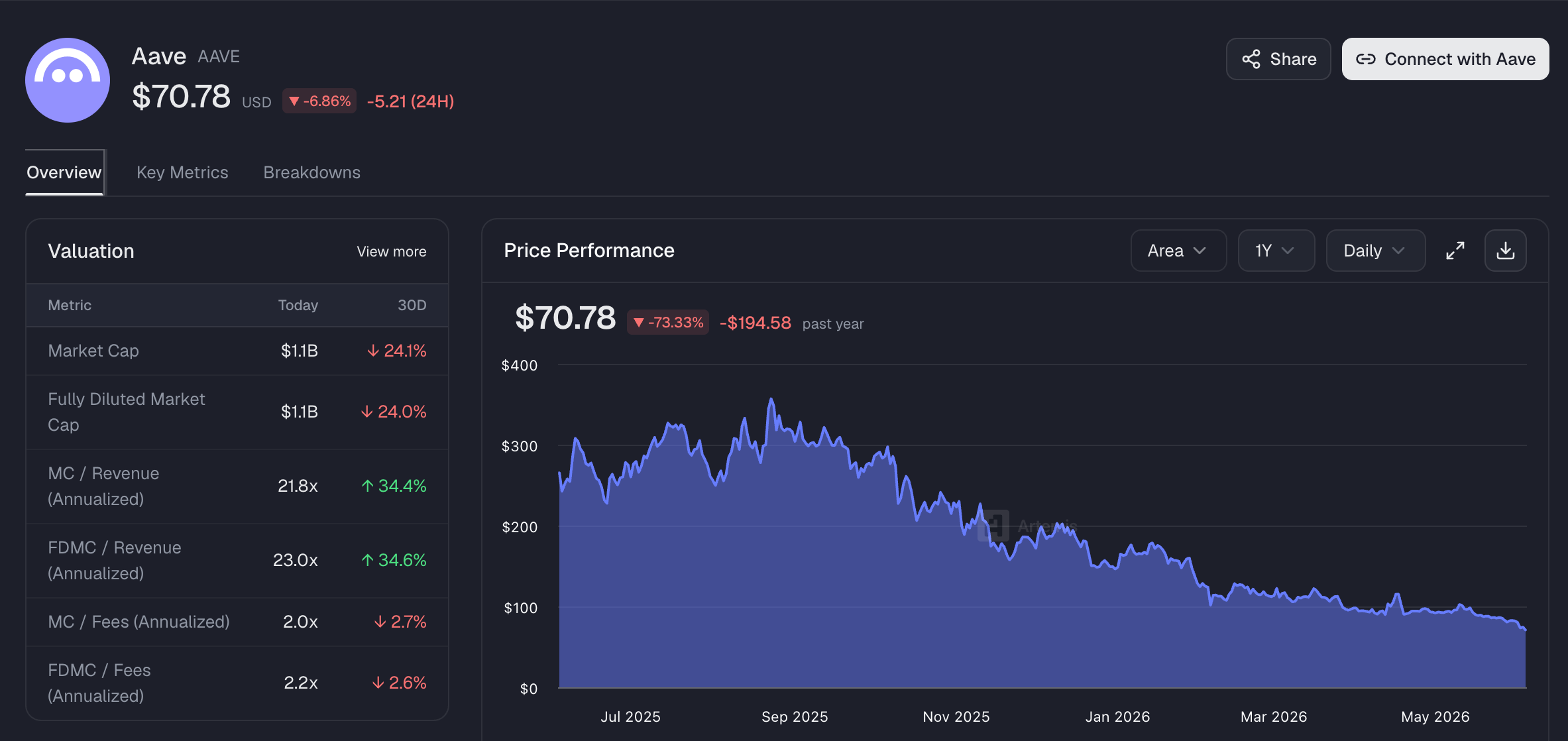

6. Fair Value Range

Our rough fair value range:

$120 – $170

This is a range based on the base case from our investment memo.

The assumptions:

Aave keeps a relevant share in DeFi lending.

TVL stays above $20B and grows gradually.

Fees normalize around $500M–700M.

The $50M buyback budget remains sustainable.

Supply risk stays low because AAVE is already mostly diluted.

The market starts valuing AAVE as a blue-chip DeFi cash-flow protocol, not only as a governance token.

7. Scenario Range

Floor value: $48

This assumes:

TVL falls below $15–18B;

annualized 30-day fees become the better indicator of the new run-rate;

Morpho and Spark compress Aave’s growth and pricing power;

buybacks are reduced or used more for ecosystem funding than token scarcity;

AAVE remains governance-heavy, not cash-flow-accretive.

Base value: $145

This assumes:

Aave keeps a relevant share in DeFi lending;

TVL stays above $20B and grows gradually;

revenue is enough to fund the $50M buyback budget and DAO initiatives;

supply is almost fully diluted;

the market values AAVE as a blue-chip DeFi cash-flow protocol, not just a governance token.

Bull value: $378

This assumes:

Aave captures a growing share of onchain credit;

GHO and V4 improve monetization;

protocol revenue becomes more stable;

buybacks become materially accretive;

the market assigns higher multiples to DeFi protocols with real revenue.

8. Buy Zone

$60 – $85

At today’s price, AAVE is inside the Attractive Zone.

At this level, the setup offer:

Better downside protection

More attractive expected return

More room for estimate error

A cleaner margin of safety

9. Margin of Safety

Margin of Safety: Adequate

For an investor willing to accept protocol risk, token risk, and DeFi cyclicality, the margin of safety is adequate.

To get a strong margin of safety, we would want either:

Price below $65

Stronger evidence of permanent buybacks

Sustainable net revenue

GHO growth

Better token value capture

Stable market share against Morpho and Spark

10. Expected Value

Bear case

Fair value: $48

Probability: 30%

Base case

Fair value: $145

Probability: 50%

Bull case

Fair value: $378

Probability: 20%

Expected value:

EV = (30% × $48) + (50% × $145) + (20% × $378) ≈ $162.50

→ +129% upside from the current price

Expected Value: Positive

11. Final Takeaway

Aave is one of the highest-quality DeFi protocols, with real usage, real fees, deep liquidity, and improving token economics. But the main risk is still value capture: protocol success does not automatically equal token-holder return.

This article is based on:

Token Terminal, Artemis, DefiLlama for financial data, valuation metrics, historical figures, and market data.

The valuation ranges, scenario probabilities, and expected value estimates are not precise forecasts. They are working models. They may be wrong.

The valuation process uses AI to combine multiple investment frameworks, financial inputs, and decision principles. This can improve structure and consistency, but it does not remove uncertainty, judgment error, data limitations, or model risk.

All conclusions should be treated as provisional.

If you enjoyed this issue, support the project with a ❤️ and share it.

Follow along:

X: Monta Capital

LinkedIn: Luca Montanari