Research Note #05 — Doximity

A study of quality, price, odds, and sizing.

Some ideas deserve attention before they deserve capital.

This series is where we study one asset at a time, define the risk, and decide what price would make the bet worth taking.

This is not financial advice.

This week’s Research Note is about:

Doximity — DOCS 0.00%↑

1. Why We Are Watching It

We are watching Doximity because it sits in an interesting place.

It is not a hospital system of record like Epic or Cerner.

But it is also not just a simple content app.

It is closer to a system of work for doctors: communication, fax, tele-health, scheduling, clinical information, and now AI tools.

We are watching it because:

It has strong doctor reach.

It generates real cash.

AI risk may be overstated.

The stock still trades below our base value.

The key debate is not quality. It is durability and monetization.

The simple thesis:

Doximity is a high-quality, cash-generative healthcare software business where the market may be over-discounting AI disruption, but the moat is not perfect because Doximity does not control the clinical record.

The key question:

Can Doximity remain relevant in the daily workflow of doctors and turn AI engagement into durable revenue?

2. What It Does

Doximity is a digital platform for U.S. medical professionals.

Doctors use it for:

clinical news

professional profiles

secure communication

fax and messaging

tele-health

on-call scheduling

clinical AI tools

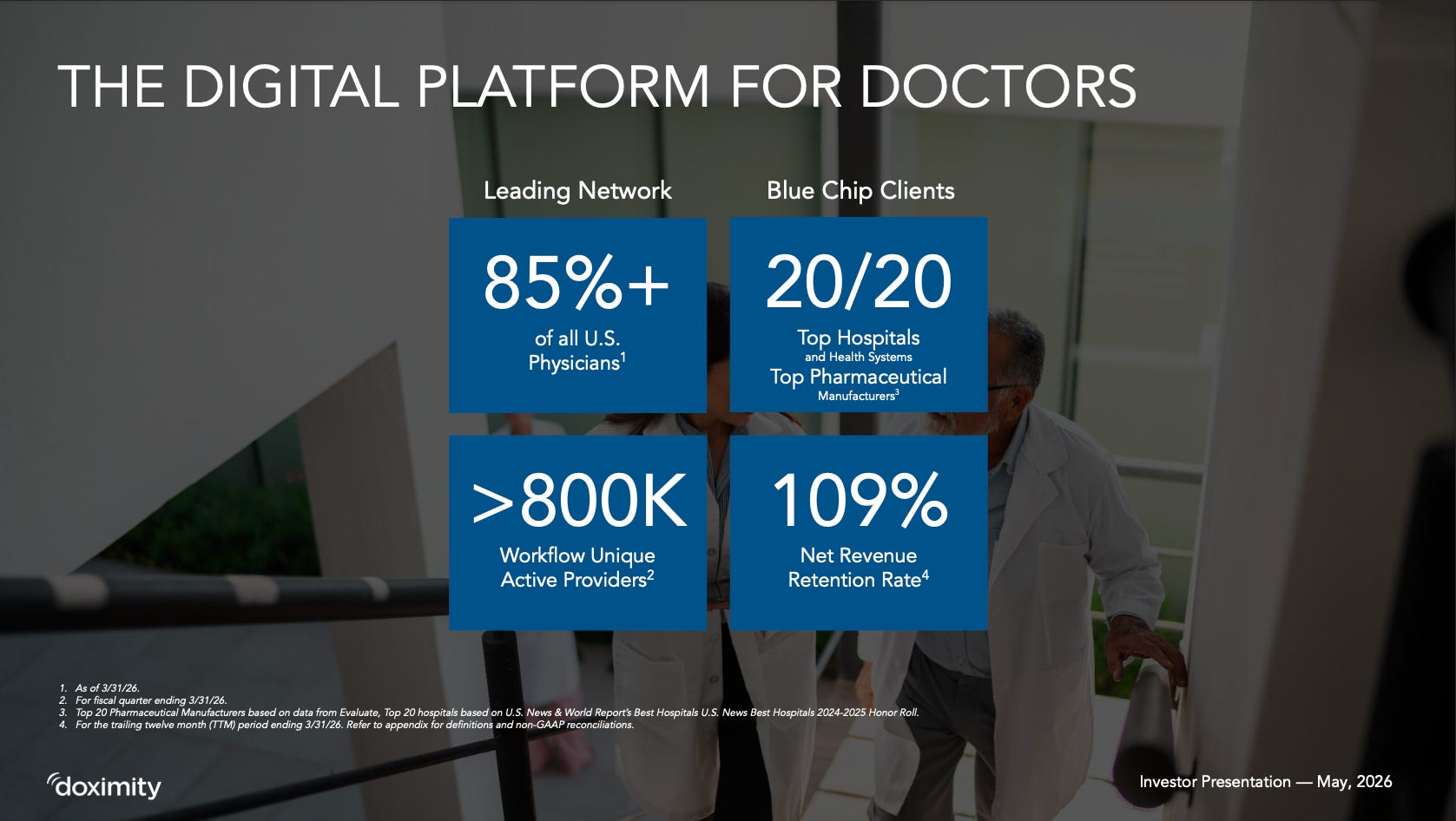

Doximity says it reaches 85%+ of U.S. physicians and has over 800,000 workflow unique active providers.

It makes money mainly through:

Marketing Solutions for pharma and health systems

Hiring Solutions

Workflow tools and platform services

The largest revenue driver remains Marketing Solutions, sold through a subscription pricing model based on audience, audience size, and modules.

3. What We Like

The attractive parts:

Strong doctor reach: Doximity has a verified professional network that is hard to rebuild from zero. The network is not just a list of users. It is a specialized audience in a regulated market.

Workflow relevance: the most important part of the thesis is workflow usage. Doximity is not only a newsfeed. It has tools for dialer, fax, messaging, AI, scheduling, and clinical support. Doximity’s own definition of workflow active providers includes usage across these tools.

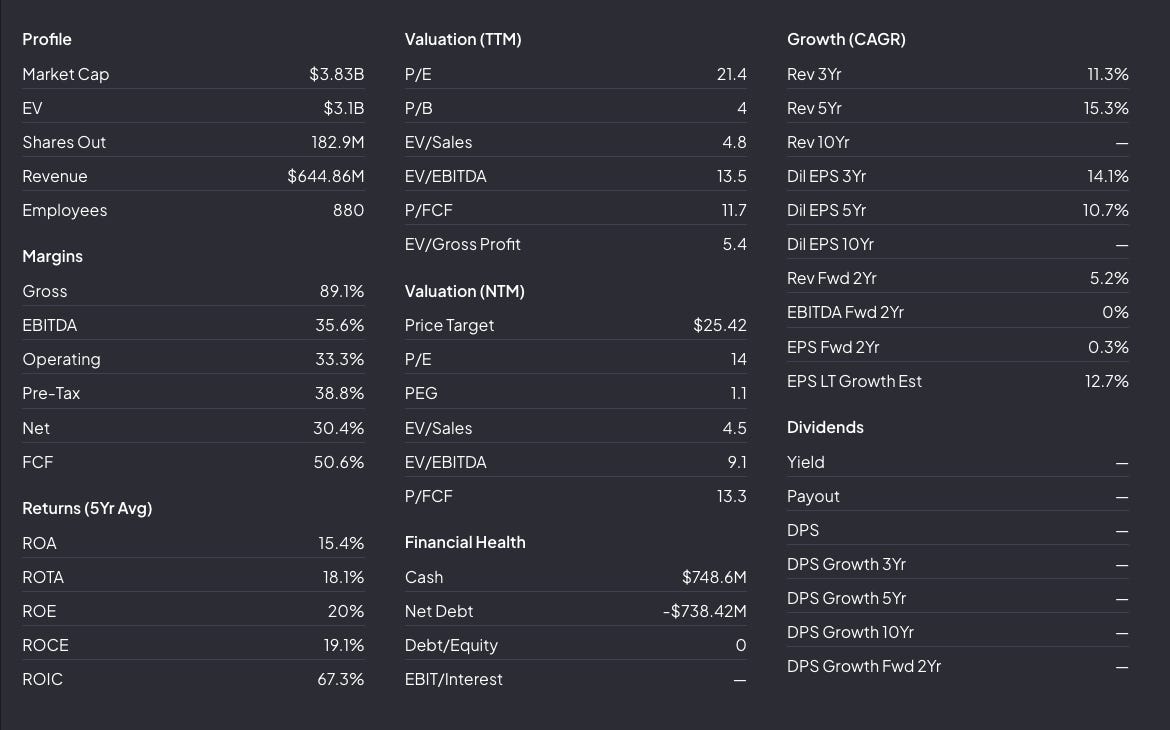

Excellent software economics: FY26 revenue was $644.9 million and adjusted EBITDA was $357.8 million, with an adjusted EBITDA margin around 55%. Stock-based compensation also rose to $121.6 million, which matters for normalized cash earnings.

AI may be helping, not hurting: Doximity reports strong engagement across news, workflow, and AI. Its presentation shows >1 million news QAU, >800,000 workflow QAU, and AI usage by about half of workflow QAU.

What we’re really looking for:

A durable workflow asset with strong cash generation, a reasonable price, and clear rules for when the thesis is wrong.

4. What Scares Us

The risks:

It is not a system of record: Doximity does not own the core patient record. That limits the moat. If EHRs or integrated clinical platforms absorb messaging, scheduling, documentation, and AI assistants, Doximity could remain useful but become less essential.

Marketing is still the main revenue engine: the workflow story is attractive, but the largest revenue driver is still Marketing Solutions. If pharma budgets weaken, move in-house, or shift to cheaper AI-native channels, the business could lose some pricing power.

AI cuts both ways: AI can increase utility. But it can also reduce the value of content, search, and some communication layers. If a good-enough AI assistant lives inside the EHR, Doximity’s usage could migrate.

SBC is high: Free cash flow is strong, but stock-based compensation is not free. We should haircut reported FCF when valuing the business. The uploaded FCF framework also warns that stock-based compensation should be treated as a real cost because it dilutes shareholders.

5. Quality Score

Business Quality — 4/5

Strong doctor network

Good vertical focus

Useful workflow layer

Not a system of record

Marketing exposure limits the moat

Financial Quality — 5/5

High margins

Strong free cash flow

Net cash balance sheet

Low capital intensity

Excellent software economics

Management / Execution Quality — 3/5

Strong execution history

Good product expansion

AI adoption looks promising

SBC needs monitoring

Monetization path is not fully proven

Total Score

12/15

6. Fair Value Range

Our rough fair value range:

$24–$35

We are using normalized free cash flow per share plus partial excess cash, not a pure revenue multiple because Doximity is already profitable and cash-generative.

7. Scenario Range

Bear value: $16

This assumes:

FY27 growth reset lasts longer than expected.

AI usage does not monetize.

Marketing Solutions faces budget or pricing pressure.

EHRs absorb more workflow value.

The market applies a lower multiple to Doximity’s cash flows.

Base value: $30

This assumes:

Doximity remains relevant in doctor workflow.

Growth is slower but stable.

FCF remains strong.

AI improves engagement, but monetization is gradual.

The market values the business at a reasonable FCF multiple.

Bull value: $39

This assumes:

AI becomes a real workflow and monetization layer.

Pharma and health system customers expand spend.

Doximity proves it is more than a marketing channel.

Margins remain strong.

The market rerates the stock without needing euphoria.

8. Buy Zone

$18–$22

At today’s price, Doximity is still inside the buy zone.

The cleanest add zone is still below $20.

9. Margin of Safety

Margin of Safety: Adequate, but narrowing

The stock still trades below our base value and below the low end of our fair value range. But the move from the recent lows has reduced the asymmetry. The business did not get worse. The price just became less attractive.

10. Expected Value

Bear case

Fair value: $16

Probability: 30%

Base case

Fair value: $30

Probability: 50%

Bull case

Fair value: $39

Probability: 20%

Expected value:

EV = (30% × $16) + (50% × $30) + (20% × $39) ≈ $162.50

→ ~ +32% upside from the current price

Expected Value: Negative

11. Final Takeaway

Doximity is a high-quality healthcare software business with strong cash generation and deep doctor reach, but its moat is not perfect because it does not own the clinical record.

This article is based on:

Fiscal.ai for financial data, valuation metrics, historical figures, and market data.

Doximity Investor Relations for company-reported results, shareholder materials, business updates, segment commentary, capital allocation details, and management disclosures.

The valuation ranges, scenario probabilities, and expected value estimates are not precise forecasts. They are working models. They may be wrong.

The valuation process uses AI to combine multiple investment frameworks, financial inputs, and decision principles. This can improve structure and consistency, but it does not remove uncertainty, judgment error, data limitations, or model risk.

All conclusions should be treated as provisional.

If you enjoyed this issue, support the project with a ❤️ and share it.

Follow along:

X: Monta Capital

LinkedIn: Luca Montanari